Azlan Othman

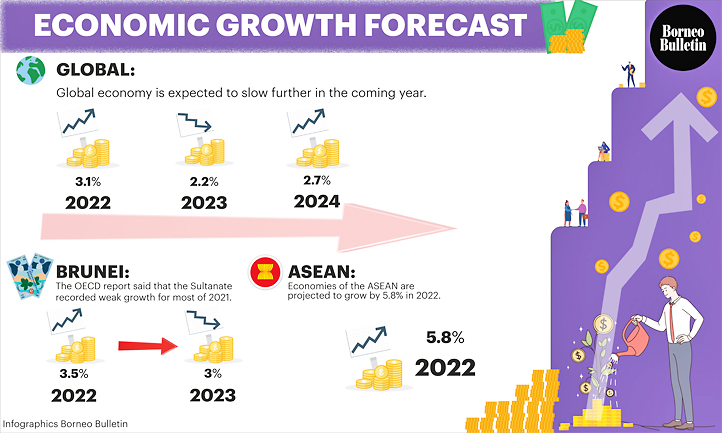

The global economy is expected to slow further in the coming year as the massive and historic energy shock triggered by the war in Ukraine continues to spur inflationary pressures, sapping confidence and household purchasing power and increasing risks worldwide, according to the Organisation for Economic Co-operation and Development’s (OECD) latest Economic Outlook.

The recently published Outlook highlights the unusually imbalanced and fragile prospects for the global economy over the next two years. The global economy is projected to grow well below the outcomes expected before the war – at a modest 3.1 per cent this year, before slowing to 2.2 per cent in 2023 and recovering moderately to a still sub-par 2.7 per cent pace in 2024.

Growth in 2023 is strongly dependent on the major Asian emerging market economies, who will account for close to three-quarters of global GDP growth next year, with the United States and Europe decelerating sharply.

For Brunei Darussalam, the OECD in its report said that the Sultanate recorded weak growth for most of 2021, and is set to grow by 3.5 per cent in 2022, followed by three per cent in 2023. The economies of the Association of Southeast Asian Nations (ASEAN) countries are projected to grow by 5.8 per cent in 2022.

Meanwhile, the recent report also said persistent inflation, high energy prices, weak real household income growth, falling confidence and tighter financial conditions are all expected to curtail growth. Higher interest rates, while necessary to moderate inflation, will increase financial challenges for both households and corporate borrowers.

Inflation is projected to remain high in the OECD area, at more than nine per cent this year. As tighter monetary policy takes effect, demand and energy price pressures diminish and transport costs and delivery times continue to normalise, inflation will gradually moderate to 6.6 per cent in 2023 and 5.1 per cent in 2024.

During a presentation of the Outlook, OECD Secretary-General Mathias Cormann said, “The global economy is facing serious headwinds. We are dealing with a major energy crisis and risks continue to be titled to the downside with lower global growth, high inflation, weak confidence and high levels of uncertainty making successful navigation of the economy out of this crisis and back toward a sustainable recovery very challenging.

“An end to the war and a just peace for Ukraine would be the most impactful way to improve the global economic outlook right now. Until this happens, it is important that governments deploy both short- and medium-term policy measures to confront the crisis, to cushion its impact in the short term while building the foundations for a stronger and sustainable recovery.”

The OECD points to substantial uncertainty surrounding the economic outlook. Growth may be weaker than projected if energy prices rise further, or if energy supply disruptions affect gas and electricity markets in Europe and Asia.

Rising global interest rates may put many households, firms and governments under greater pressure as debt service burdens rise. Low-income countries will remain particularly vulnerable to high food and energy prices, while tighter global financial conditions may raise the risk of further debt distress.

Against this backdrop, the Outlook lays out a series of policy actions that governments should take to confront the crisis. Further monetary policy tightening is needed in most major advanced economies and in many emerging market economies to firmly anchor inflation expectations and lower inflation durably.

Fiscal support that is being provided to help cushion the impact of high energy costs should be increasingly temporary and preserve incentives to reduce energy consumption. Support measures should be designed to minimise fiscal costs and be concentrated on aiding the most vulnerable households and companies.

Managing the energy crisis will require more decisive policy support to boost investment in clean technologies, foster energy efficiency, secure alternative supplies and realign policy with climate mitigation objectives.

The cost-of-living crisis also calls for structural reforms that can have a direct effect on household incomes, ease supply constraints and reduce prices. To this end, countries should focus on policies to improve the functioning of international trade, enhance productivity, tackle gender gaps in the labour market and boost living standards.